Why Fabrication Shops Are Shifting Away from Traditional Bank Loans

What changed

Traditional banking institutions have begun to pull back from the industrial sector as regional banks reach their sector concentration caps Tzortzis Capital. While banks are tightening their belts, the broader lending environment is shifting, with credit approval rates reaching a historic high of 78% through alternative, digital-first channels Praxent.

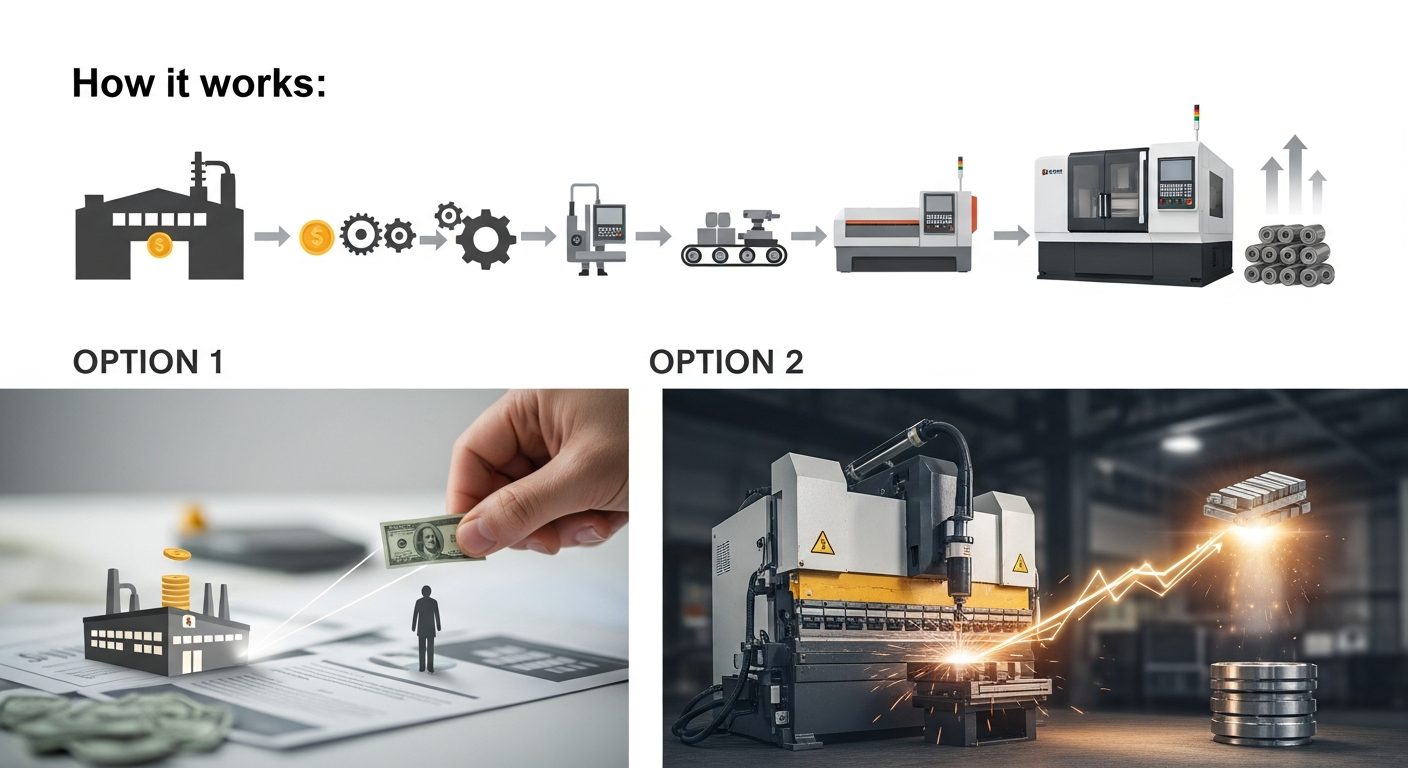

How it works

As bank credit becomes restricted, manufacturers are pivoting toward five primary non-bank structures to acquire machinery Tzortzis Capital. While both sources agree that the market is becoming more flexible, they approach the trend from different angles: Tzortzis highlights the structural shift in loan originators, whereas Praxent emphasizes that lenders are increasingly prioritizing usage-based and flexible digital products to keep approval rates high Praxent. The mechanism relies on shifting from traditional collateral-heavy bank loans to specialized equipment finance, including sale-leasebacks, which allow shops to leverage their existing balance sheets to fund new CNC or laser cutter investments.

Who it hits

This shift primarily affects small-to-mid-sized metal fabrication shops that have traditionally relied on relationships with regional banks for machinery procurement. While established manufacturers with high credit profiles are still navigating bank limits, smaller shops that were previously held back by rigid bank documentation requirements are finding more success through the flexible, tech-forward non-bank platforms emerging in the current landscape Praxent.

Why this matters for Owners and operations managers

For a shop looking to add a new five-axis CNC or a high-speed fiber laser, the move toward non-bank financing is a strategy to preserve liquidity. By using a sale-leaseback or a direct equipment finance agreement, you can deploy machinery into your shop floor immediately without tying up 20-30% of your cash reserves as a down payment. This maintains your working capital for daily payroll and materials, while the financing structure itself aligns better with the actual production capacity of the new machine.

Because non-bank lenders prioritize the equipment's value over a general bank relationship, the underwriting process is often faster. You can expect decisions in days rather than weeks, and terms are increasingly tailored to usage-based models, meaning your repayment schedule can potentially fluctuate with your fabrication volume. This agility allows you to upgrade your production capacity during periods of high demand without the long-term debt drag typically associated with conventional bank equipment loans.

Bottom line

Regional lending caps have made bank financing for machinery increasingly difficult, but non-bank alternatives are offering record-high approval rates. Leveraging these flexible structures allows you to scale your fabrication capacity while keeping your cash reserves intact.

Check your financing rates here.

Disclosures

This content is for educational purposes only and is not financial advice. metalfabricationfinancing.com may receive compensation from partner lenders, which may influence which products are featured. Rates, terms, and availability vary by lender and applicant qualifications.

What business owners say

4.9-

This company was lightning fast and the experience was amazing. Thank you, Dan — you're a real pro!

-

Good service Joseph Krajewski is the best agent ever. He provided excellent service. I strongly recommend working with him if you have the opportunity.

-

They gave me a chance when nobody else would. I'm very satisfied.

Frequently asked questions

Why are regional banks pulling back from equipment loans?

According to Tzortzis Capital, many regional lenders have reached sector concentration limits, forcing them to restrict new capital for manufacturing.

Are credit approvals actually harder to get right now?

Contrary to the tightening of bank credit, Praxent notes that credit approvals remain at historic highs of 78% due to the rise of digital-first lenders.

What is a sale-leaseback?

It is a financing structure where a shop sells existing equipment to a lender to unlock immediate cash, then leases the equipment back to continue production.

- Industrial Machinery Lease vs Buy 2026 Guide for Fabrication Shops (20/06/2026)

- Kentucky Used Metal Fabrication Equipment Financing and Leasing (19/06/2026)

- Kentucky No Money Down Metal Fabrication Equipment Financing (19/06/2026)

- Kentucky metal fabrication equipment financing for bad credit shops (19/06/2026)

- Kansas Metal Fabrication Equipment Refinance (19/06/2026)

- Kentucky Startup Metal Fabrication Equipment Financing and Leasing (19/06/2026)

- Kansas Metal Fabrication Equipment Financing That Fits Real Shop Timelines (19/06/2026)

- Kansas Used Metal Fabrication Equipment Financing (19/06/2026)